*TeachersRetire is not affiliated with, endorsed or sponsored by PSERS*

PSERS Options 2 and 3 are very similar so we will cover both in this article. Each of these options provides lower monthly pension payments than the Maximum Single Life Annuity and Option 1. The benefit of selecting an option with a lower monthly payment is much better protection for your spouse if you pass away. That is the case with Option 2 and 3; a more certain and lasting death benefit in exchange for a lower pension payment. PSERS members who want their surviving spouse to have dependable income for life usually select one of these options.

What happens with Option 2 and 3 when I die?

Pension Options 2 and 3 are quite simple. There is no Present Value calculation as with Option 1 and there is no choice that leaves you with no death benefit at all like the Maximum Single Life Annuity. When you apply for retirement with PSERS and select one of these options, you receive the monthly payment as it was quoted on your Retirement Estimate. The monthly payment depends on your age at retirement and that of your beneficiary (called a survivor annuitant). In general, the younger you and your survivor annuitant are at retirement, the lower your payment.

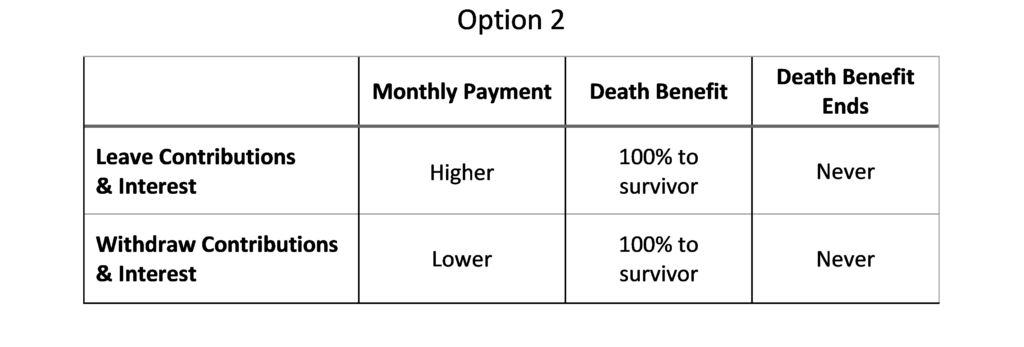

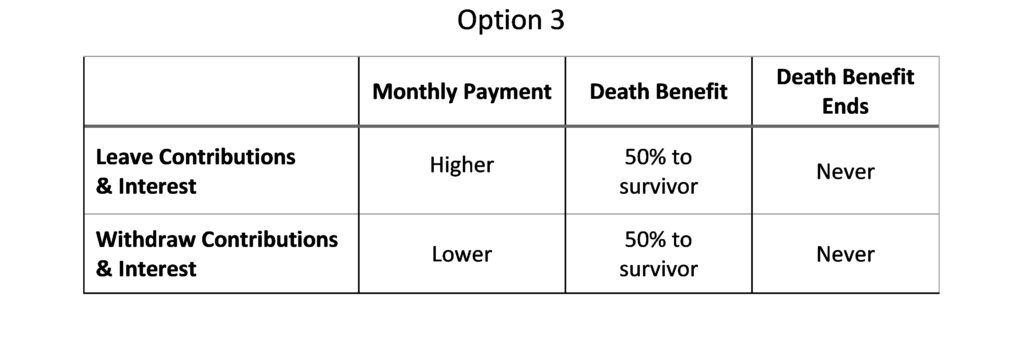

If you die before your spouse, Option 2 allows them to continue your pension payment for the rest of their life. Option 2 is often called “100% to Survivor” for this reason. Option 3 will provide them with half of your pension payment for the rest of their life. Option 3 is often called “50% to Survivor”.

Unlike the Maximum Single Life Annuity and Option 1, you cannot outlive your death benefit period. Whether you die one year or thirty years after retirement, your survivor annuitant will continue receiving all or half of your pension.

Since Option 3 leaves less of your pension for your survivor, the monthly payment is higher than that of Option 2.

Can I still withdraw my contributions and interest?

Yes. As with all of the pension options, you can choose to withdraw all or a portion of the contributions and interest in your PSERS Account. You can find the balance in your PSERS Account on Page 2 of your Statement of Account or by logging in to the Member Self Service Portal. Learn the pros and cons of withdrawing your contributions and interest here.

If you withdraw money from your account at retirement, your monthly payment for Options 2 and 3 will be lowered. This does not change the continuation of the pension for your survivor. The payment will simply be lower from the start.

Is pension Option 2 or 3 right for me?

Option 2 is likely the most popular choice for PSERS retirees who are married. The security in knowing that your spouse will continue to receive your full pension after you die is very comforting. It also makes retirement financial planning much easier as you will know how much income your spouse will receive each month. This can help you have more clarity when making decisions about Social Security, long-term care, investments, life insurance and many other important retirement considerations.

Option 3 might be a good choice for someone who is married, wants to make sure that their spouse continues their pension but also needs a little more income each month right now. It could also make sense if your spouse has their own pension and they won’t need all of your monthly payment after you pass away.

The bottom line when considering your pension options is to make sure that your spouse is in the best possible financial situation if you die first. Many people find peace-of-mind with either of these options knowing that there will be income left for them that they can’t outlive.